*free to use from https://unsplash.com/photos/1I811IkRlKE

The banking industry has performed under the same model since industrialisation. Despite the pressure to shrink the branch system in the past nine years due to the growth of digital banking, branches have clear advantages (EY, 2017). Physical locations allow to build trust and credibility, provide face-to-face advice, convenience and transition to digital services. But with digital channels being much more cost-efficient, is it effective to operate both digitally and physically?

Digital banking moves the financial relationship between the bank and customer purely to technology. The major advantages of digital in this sector is that its efficient, mostly error-free and cheap compared to the branch network. The increased use of technology and its convenience makes it impossible for the banking industry to stay away. Without online banking a lot of customers would go elsewhere, and therefore, it’s important to stay ahead of competition in this market (Marous, 2016). However, even with these high-valued benefits there are downfalls to being just digital as a bank. Automation takes away the personal experience when considering the customer service, complaints and financial advice. The Global Digital Banking Report (2017) warns that digital-only banks lose their appeal. 24% of UK users have dropped their appetite for this stream of banking. This is mostly due to the lack of personal touch and privacy and security concerns. Nevertheless, daily digital banking use has increased globally (RFi Group, 2018). It is clear, that digital operations are important but aren’t as efficient in this sector without physical operations.

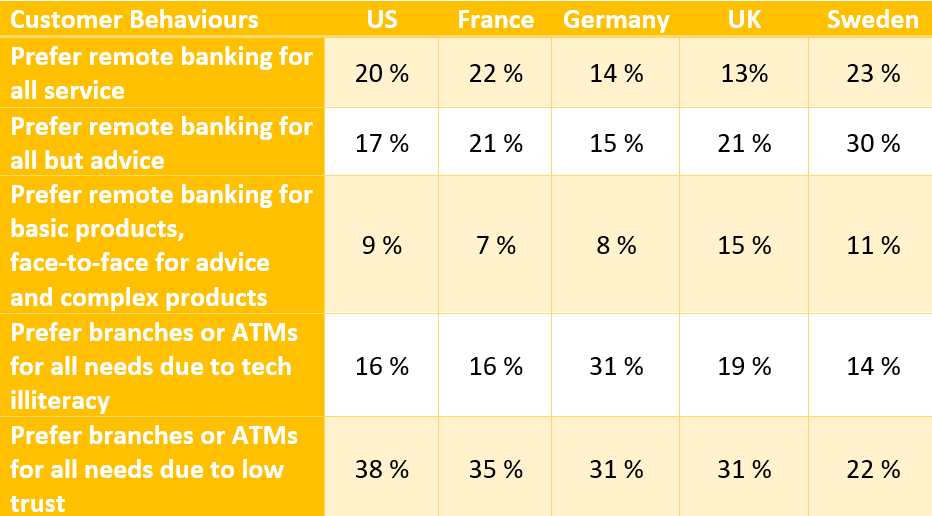

Despite the advantages of combined efforts of operation, there are distinct disadvantages to branches. They are expensive to operate, adding up to about half of the operating costs of a bank. Even though they provide customer experience through customer service, its often hard to ensure a consistent experience across branches. The uneasy global financial situation puts pressure on banks to devise their strategy. The big question is: Do they invest into branches to create a positive brand image and greater trust with consumers but pay at least double the price; or do they save money and invest in the growing, less-expensive digital operations but lose their personal and unique touch with the customer. A recent survey in 2016 found that most of consumers would still like to see branch presence within banks. On average, only 19% of customers prefer an all-digital experience (McKinsey & Company, 2017). Figure 1 shows a more detailed breakdown of consumer behaviour towards digital and physical operations.

At the moment, even though banks on a whole have increased their digital presence by following technology trends in the industry, they have still not fully found a way to transform their branches to support their online presence (EY, 2017). Currently, most of the efforts are focused on closing underperforming branches and installing more ATMs and, in some instances, opening mobile branches. However, in order to create a wholesome ecosystem between branches and online banking, banks need to address slightly different branch issues. Branches need to address costs, physical customer experience and reasons to visit a bank in the first place. As most branches have been around for a while, they would be more spacious than needed and employ more staff to look after these spaces and operations. By potentially selling off extra space and employing only the minimum number of staff required, can reduce the operating cost of a branch. By investing in skilled staff training, as well as, branch perks and interior, the banks can strive to ‘automate’ experiences across branches (McKinsey & Company, 2017). Banks also need to make sure that some parts of financial services stay available only at branches to create a need to use them. Getting cash out or putting large amounts of cash in should stay a branch operation and not only would that increase footfall into the branch but will also increase security that consumers are afraid online banking might be taking away.

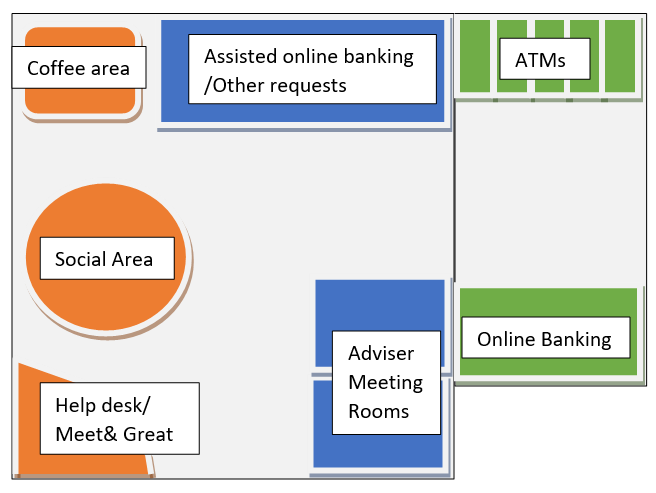

As we have established here, neither form of operations can work for a bank on its own. It is therefore, very important to create a collaborative ecosystem for digital channels and physical branches of banks. Figure 2 shows what in my opinion a collaborative branch should look like, not just to improve customer trust and experience, but also to advertise and underpin the digital services a bank provides.

In conclusion, the increase in online banking isn’t going to put a stop on bank branches, but it is rapidly making the current branch model obsolete. I believe that branch closure will still need to go ahead, however leaving enough around to have good area coverage. The branches which are left will need to be transformed to interactive, digital and customer service lead spaces for consumers. The new branch model will incorporate and support the vast advantages of digital banking as well as build trust, credibility and advice – revealing new sources of value for the banking industry.

References:

EY. (2017). Global Banking Outlook 2018: Pivoting toward an innovation-led strategy. Retrieved from https://www.ey.com/Publication/vwLUAssets/ey-global-banking-outlook-2018/$File/ey-global-banking-outlook-2018.pdf

Marous, J. (2016). Digital Banking Report: 2017 Retail Banking Trends and Predictions. Retrieved from https://thefinancialbrand.com/wp-content/uploads/files/Retail_Banking_Trends_Predictions_2017.pdf

McKinsey & Company. (2017). The future of customer-led retail banking distribution. Retrieved from https://www.mckinsey.com/~/media/mckinsey/industries/financial%20services/our%20insights/the%20future%20of%20customer%20led%20retail%20banking%20distribution/the-future-of-customer-led-retail-banking-distribution-2017.ashx

RFi Group. (2018). Banking sector continues to evolve as digital-only banks are losing appeal globally: RFi Group. Retrieved February 7, 2019, from https://www.rfigroup.com/content/media-release-banking-sector-continues-evolve-digital-only-banks-are-losing-appeal-1

Hi! This is an excellent example of an industry that has changed over the last few years. Personally, I usually use the option of online Internet banking and the mobile banking service to manage my banking and I tend to go to the bank once in a while physically. To add more to your blog, what I would like to say is that recently when I have gone inside a few different banks then I have noticed that there is a small amount of staff and there are more self-banking points/stations for customers to use which links back to the point that you have made in your blog that banks have limited staff and have reduced physical bank locations and that they are becoming more digitised.

LikeLike